Hello, Mahmoud. Good morning, Natu. How are you? Good. Happy Friday. I’m, I’m just, uh, happy Friday. Nice. Yeah. Yeah, just a lot of, um, back and forth here. A lot of people are, sometimes it’s quiet and then sometimes everybody comes at the same time, so we’re helping everyone out. Alright, so I saw the last email and, uh, yeah, I changed it to Green Arrow Capital on the press, so I saw that.

Yeah, because that’s a, the vehicle that I, uh, gonna use, uh, this, uh, capital for. Okay, perfect. So yeah, what we can do, we can also, we can just go through everything and then just see where everything is at. Uh, you said you’re, you’re going, uh, when do you come back from, uh, uh, uae? Uh, I’m, I’m planning to stay at least like, uh, between four to six weeks.

Okay. That’s a while. We got it. Nice. Yeah. Okay. So let me pull up all the information.

Actually, I w um, I’m going to the UAE for only one week, uh, for investor conference there. And then, uh, from there going to Australia and supposedly, uh, we’ll be able to close my first acquisition there, but, nice. The, the guy I, uh, I hired to help me with the finance came back to yesterday and said, The, the Financeer, uh, is backing out and, and they require me to put a, a deposit, big deposit, like 30% deposit of the precious price.

So I was, I was pissed off because I was looking for like, monthly course, uh, loan or, or debt, so that it would be, the loan would be based on the merit of the business itself, not based on my, my own merit. And, uh, they said, well, we, we cannot find someone to do this, uh, like investment bank or something. So I kind of like pissed me off.

So I, I’m back in a square one to fund this acquisition, and I was supposed to go on and close the deal already. Everything was worked out, but, uh, it’s, it’s, uh, I have, uh, looks like I’m, I’m having a hard fi hard time finding a local party trusted party that it can. Close a deal for me in terms of funding and finance.

Mm-hmm. Was this an investment? This was an investment bank, you said? Uh, no, it was a traditional investment like, uh, equipment finance and, uh, the account receivable finance. Okay. And, uh, so they, they back out and unless I, I put at least 30% down, said, well, this is, this is kind of like a financing. I mean, why, why should I, if you think that this is, the equipment is, is good enough to be funded and they account receivable, why should I put down, uh, a deposit the 30% deposit so that you can, he can give me 70% amount of value.

Uh, it doesn’t make sense to me. So, yeah, it’s just like a normal, it’s like a real estate. It’s like worse than a real estate deal. Um, yeah, exactly. Yeah. Yeah, what, what we can do, uh, I guess what I can control on my side, I, I can just, uh, I guess for the next projects we’ll just give you some more people, let’s say, let’s say in the next few days, five introductions and then one of them are going to be really good and just so you can have somebody just like, yeah, I think you already have a good network, but I think we just want to get some more people on backup as well.

Um, yeah. You know, just so we, we don’t get into this situation, but, but okay. So thanks for the update and, uh, and you know, hopefully deal with that. So are you going to, so are you gonna now work on that capital raise at the same time as we’re working on this one right here? Yes. Okay. Uh, what? Yeah, we have to have to, yeah, we have to go keep moving, basically keep for marching forward in both fronts.

Uh, I already bought the tickets and, and make, uh, I reserve ticket that flight reservations and everything, so I, I have to go anyway. So yeah. Regardless whether I’ll be able to close the deal or not, maybe I’ll make introductions there, but that will, will, will have to go forward at the same time, uh, trying to find, uh, some, uh, date financer somehow, uh, along the way.

But, uh, I wanna also, uh, continue with the, with the raising capital for global financials. Yeah. Uh, I, I, I made, uh, a software offer yesterday. Mm-hmm. Uh, to them, I’m offering, I offered them, uh, 32 like equi the enterprise evaluation of about 32 and a half. And I offered them 60% at closing and the rest over like five, six years.

I know that they, they probably don’t like that, but I’m hoping that they can come back and counter offer so I know where they are and what they are looking for. So I loop all the offer, uh, to them to see where they stand and whether they take it or not, and, and go from there. I’m willing them to, to give them more based on, uh, the raising that we cannot do, uh, for the acquisition.

Uh, just give them more at closing. Uh, but, and, and, and less, uh, deferred payments. But, uh, I, I gotta, I gotta know where they stand first, and that’s why I send them the soft offer. Once, once we finalize everything, then unlock the deal in l o i, and, and we pursue, uh, in the, uh, in the raising efforts. Yeah, now’s a good time to really start pushing the raisin.

Exactly. Because, uh, I’m assuming with your offer, you’re probably going, your offer is probably like, you know, maybe they’ll say, let’s say that they say no two times and then we, you still get a decent offer. Uh, maybe they’ll say something like 80% of 60%, but then maybe if you weren’t that aggressive, you wouldn’t be able to do it.

Well, I mean, we do it too. Like we, we just say, even for our product, we’re just like, oh, you know, our price is, like we say, our price is like 10,000 and then, and then really the price is 5,800, but then, or like 5,300. But then, you know, we just do that just so that people negotiate back and then really it’s like, oh, it’s like, it’s a price.

Mm-hmm. So it’s just to get people to that middle state, so it makes sense. That’s right. Yeah. Yeah. Just, just to keep the ball rolling, uh, basically. And, uh, try to accommodate as much as we can from their side. And, uh, If it doesn’t work, it doesn’t work. But if, if it works, we, we make it work. Uh, e exactly.

One, one more, one more important thing. Uh, so then, because you, so I know a good friend in Palm Springs in business partner, he, he knows, he knows a lot of the investor conferences. Um, so like, he knows which ones are good and, and so like, he’s, he and he, he’s been scammed for like hundreds of thousands of dollars and then he’s gone to really real ones and really good ones.

So, um, so which one are you, are you happening to go to, just so I know, just so I can, um, in case I heard of it in Dubai, uh, yeah, yeah. There is a, there is a guy, uh, who sell courses for buying, uh, uh, uh, buying, uh, businesses, uh, that is in the brink of, uh, bankruptcy. And he has his strategies and, and his selling courses.

I took this course a long time ago, and, uh, everyone, uh, every year or every other year, he, he makes a conference in throughout the whole world. Like sometimes in Boston, sometimes in Miami, sometimes in Dubai, sometimes in Singapore. So, uh, I haven’t attended any of his courses since the first one, so now he’s doing it in Dubai.

It’s called Deal Fest Dubai. Ah, with the Harbor Harbor Club. Yeah. And, uh, and that’s what I’m, uh, planning to attend. Nice. Okay. In, in his, uh, in his conference, uh, in his de the in meeting, a lot of investor comes in and a lot of, uh, people that interested to buy businesses come in to learn his, uh, techniques and methods and, and, and modeling and stuff like that.

So you could, you, you go there and you meet a lot of people, like-minded people, and, and, uh, of course there’s a lot of financiers and funders, uh, VCs and PEs, uh, attend as well to try to catch a good deal. So hopefully, we’ll, we’ll meet some, uh, over there that could be interested in what we are doing here.

Nice. Yeah, that one sounds good. I’ll talk to my, my associate. I haven’t heard, I’ve heard good things about that one. I heard about it a few times. Uh, so I haven’t heard any big complaints, but, um, and you, you already know, but, so that’s good. So, okay, so, so let me, let me go through and present what we got, uh, together and then we can make any finals.

So today we can also make some changes as well. Uh, yeah. You know, before we start doing some, we can do some introductions on our side as well, uh, when the time is right. And we can do it today, or we can do it Monday. Uh, depend. But probably Monday is probably better because, uh, everyone is, is, uh, like asleep on Friday and the weekend, but, mm-hmm.

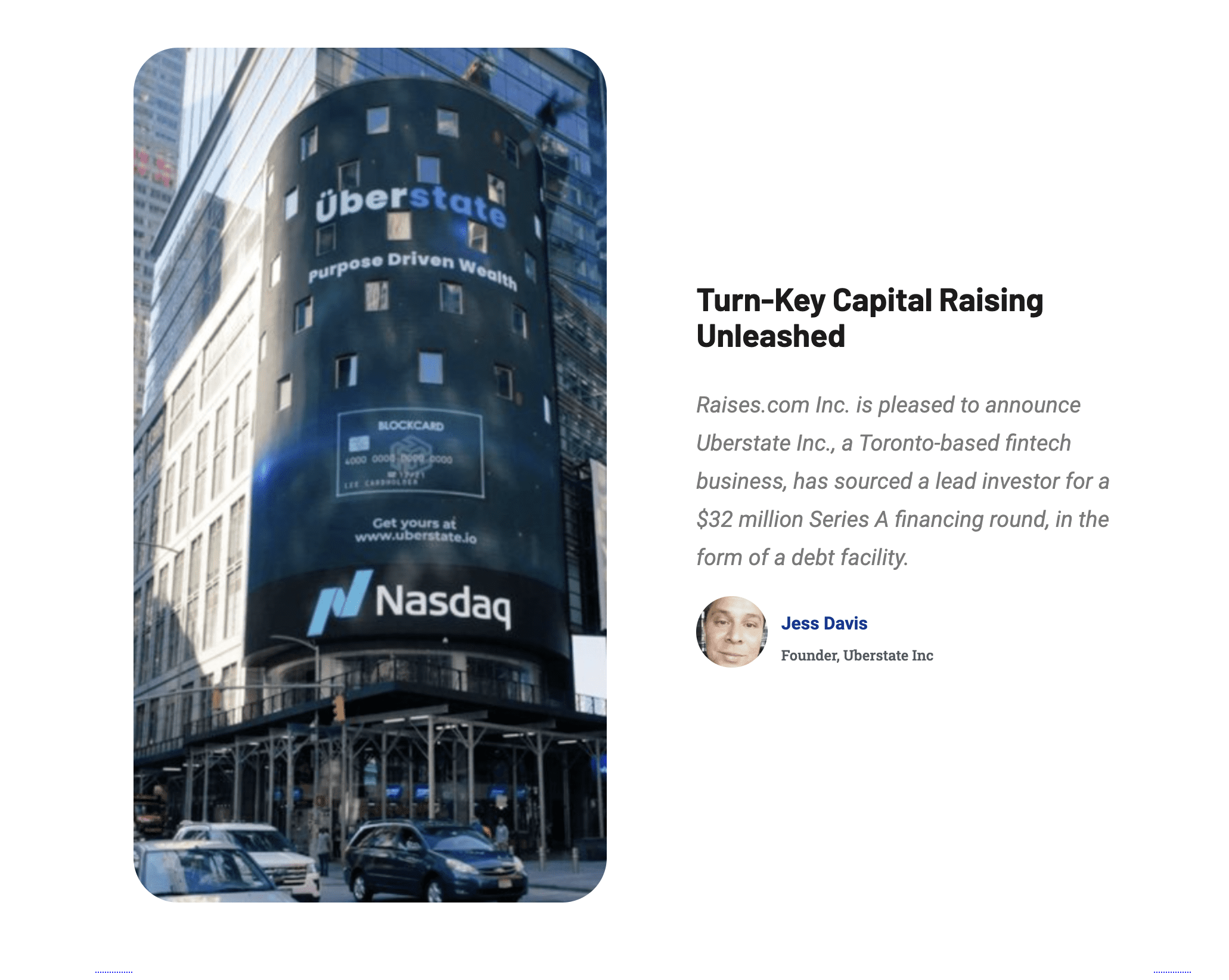

Yeah. Yeah, yeah. So then, okay, so we have the draft press release. This will go to bloomberg.com. Uh, uh, so then after that, do you have any other corrections aside from that last, um, green Hour Capital? No, that it looks good. So you plan to, uh, uh, publish it in, in Bloomberg, uh, online or how, how that will work?

Yeah. So, um, I’ll show you an example of when, um, this is one I was in a while ago. Uh, let me look at this up. Um, This was Lotus Energy. This was just another deal I worked on.

Uh, so something like this, you know, because sometimes what happens is there’s some investors that they have the email subscription to Bloomberg, and so we can go out, uh, a lot of public companies have a service where they pay, uh, to get these out to Bloomberg or Business Insider or so on. So it’s just like a little press release and people get emailed.

Mm-hmm. And also people, if they Google the deal, then they can see this on, on, on Google as well. So is this more, um, yeah, that’s, that’s cool. Yeah. This is insight thing. And then last thing, sometimes when we close deals as well, we, we, um, announce in there too just to, um, you know, just to build the credibility as well, a little bonus.

So is this, uh, like a, a free service or bid service, uh, to Bloomberg? So, I mean, we, we like, I mean, you already paid us to do it, so we’ll do it. But, um, but yeah, people can pay. I think it’s like, uh, so we have a yearly subscription and you know, we paid around, what was the price again? So it was around, what, 4,000 or something a year?

Or People can pay about between 800 to a thousand to get it themselves. Uh, and you can use access. Yeah, we use Access wire. Access Wire. Um, I think Access Wire is the best one for this. So you can do it directly to his, like access wire. But then we, we can just cover like the, like the, whatever it is. And then, uh, I see.

That’s nice. Yeah. Yeah. It’s a good service and, and good, uh, marketing tools, uh, for you guys as well. E Exactly. It really helps us out. Yeah. Okay. So we have the pitch deck, the, the pdf. This one looks better because it’s more, um, we have the PowerPoints and the pdf, the PowerPoints of it. You can, that’s the one you can edit, but.

But we took, so then we just took things from your existing pitch deck. Mm-hmm. And then we mm-hmm. Used our existing process for ours, and then we just sort of combined them. Um, so here it is. And feel free. Any feedback, I’m open any feedback just so we can get it the way that we, we like before it goes out.

Yeah. Okay. Yeah, I haven’t, I haven’t, uh, uh, reviewed that yet, but it looks good. Okay.

Now I actually have a question here. So then, because so, so because you’re raising money, if you’re raising money as a fund, I don’t know if we should, I don’t know if you should mention the, the target name. Because, because Yes. And then it’s like, it’s like, wait, and then maybe they’ll try to go around you, you know?

Yes, exactly. We, we should, we should hide the name, uh, and, and the location or anything related to it. Uh, we just mentioned the, the names, uh, uh, and, and just like service name, that, that’s pretty much it, but, uh, I shouldn’t include the name. Yeah, no, I, I agree. So I’ll take a note of that so we can fix that.

Uh, today. Uh, market opportunity problem solutions. Just a basic, uh, slide.

Oh, do, do you have, do you have like a, um, like a nice profile picture or a corporate picture we can add to the, uh, to the deck as well? Yeah, yeah, I do. I’ll, I’ll, I’ll send you, uh, my company profile. It has a good, nice picture of me there. All right, good. All right. We’ll add that as well. Uh, that’s it. It’s, it’s pretty sim pretty simple, you know, because people, we, we just notice people j their attention span is just so short that, uh, yeah.

You know, we just wanna get their attention quick. So, so, and that’s it for that one. We’ll make those changes. We have a one pager

and Yeah. Is this everything on one page? So should you add in the one pager, like the, the key, uh, metrics highlighted, like in, in bigger font or something like the, uh, I rrr, uh, and the growth and stuff like that? Yeah. I think, um, I think we actually, that’s a good point. I think we should, because. I mean, we have it in because that, that’s what attract, uh, most investors on how much is IRR that I’m expecting out of this business, how much of fund that we, we need to raise, uh, how many units and the number of units, uh, the I r r, uh, growth rate tho, those are kind of like, should be like in highlighted in a much bigger form.

I agree. I agree. We, we could, uh, the last one we had, we had the I R R. We didn’t even put it here for some reason. Maybe. I think it’s a graphic designer. We, we, but then, uh, would you like it, uh, down here or should we put this, uh, up here? So they, I think, yeah, it should be, it should be in the, in the left top corner.

Okay. Because this is the first, the first thing, the eye goes through it basically. Yeah. Yeah. I agree. So I’m gonna get that as well. So we get that there. Anything else? Uh, the rest is just like, uh, you know, most people don’t read much, uh, the text. That’s true. You wanna just get the, the key metrics. Uh, they just look at it.

You just, it takes few seconds for them to, to make a decision basically. Uh, and, and, and then if they are interested, then they will start to read the rest of the, the text, uh, and, and then start asking questions. But in, in the first glance, they, they just gonna look at the numbers and, and make calculation in their head quickly to decide whether they can, uh, read the rest of the page or not.

I agree. Yeah, absolutely. As as you said, most people have a very short attention span. Especially investors. Yeah. Handling millions of dollars and they don’t have time to read everything. Yeah, no, exactly. Yeah. So make that change for sure. All right. So we’ll get that done. Uh, we have the same, so this is just the Microsoft Word version of the same thing.

Mm-hmm. So we just need to put the, uh, so the I r this one actually has the I R R, which we, we didn’t put yet. So in the i r we said 15% is the targets. We don’t have a cash and cash return for the fund. Save and close. This is the ugly version of what is this? Uh, the, the cash and cash. Is this a separate calculation from the, the discount cash flow that we, we did?

Or this is something we can add to the calculation? We could add it. Uh, the reason why I was a bit reluctant is because, It’s very real estate, you know? So like a lot of the real estate people Oh, I see. Yeah, I see. So as it depends on the industry itself. E Exactly. And um, but then what, what, what David did, and we can always get him to do more as well.

He took this, he took the, uh, the model, and it’s just loading all the mm-hmm. Just let’s take, take a second for this to all load. But he took the model and then he made, um, uh, a limited a waterfall. Yes, exactly. Yeah. That, that was nice. Uh, I saw that. And I actually, I have a, a water model waterfall, uh, model that just can plug in the numbers and it has a nice graph to it.

I was thinking maybe you can add, uh, a graphic representation of the numbers, which will be nice to, to add as well. Okay. Will do. But, but this is something like, it’s not, it’s a minor. Yeah. It’s like a little bonus. Yeah. But again, graphic representation, it, it, it goes a long ways with investors much more than numbers.

Uh, again, that’s, that’s the first glance. The people that look at the, the graphs and if they’re interested, they will, will follow in the numbers and the spreadsheets and the models and all of that. I, I agree. I wanna show you another because, uh, I have to get the actual model to show you from Google. Uh, cuz Google Sheets doesn’t have like the, this is Google Sheets instead of Excel.

You used Excel. So that’s why it says re let me just get, yeah, I see. Yeah. So lemme just get the actual, uh,

So just one moment. I’m just in another window. Global financials.

Oh, these drafts is, uh, is uh, reference to other sales. And that’s when they messed up. Yeah. Okay. Aha. Batch file. Okay. I have it in another window. Let me stop sharing this. Share global financials. Yeah, just so we can see. It’s together. Here it is here. Yeah. So, uh, I got a question to ask you. Uh, I, I, I know that they put the general partnership is like 10% and 90% for the limited partnership.

Is that the typical for most of the deals or you said you we can negotiate that? Uh, yeah, no, with the investor now, if you have multiple investor and could you put investors in tier? Like one would be 90%, one would be 80%, one would be def different level percentage, or they all have to be the same level of percentage.

Sure. So then, well the first question Yeah, we can definitely, uh, yeah, 90 10 is, is usually a bit much, yeah. At most we usually say 80 20. And then I think, um, I think the idea is for us to go in, uh, and edit the, uh, the preference so that, and edit the pre and then end the percentages so that the model can be based on this, we can actually move that around.

But then, yeah, like I’ve seen two things. I’ve seen one, some people where they have two types of, uh, they have two types of units, almost like, almost like in a company where they have preferred like class A shares. Yeah, common, common stock and preferred stocks. Yeah. Yeah. So I, I’ve seen people do that and then they’ll entitle people to different, uh, benefits for that.

Uh, so that could work. Uh, but I’ve also seen people do it based on who invests first and who invests how much. Like, for example, if somebody, like the first investor in, I’ve seen them get a, I haven’t seen it change too much. I haven’t seen the percent change too much, but I’ve seen people get more units outta discounts, which will entitle them to more money.

Mm-hmm. Yeah. So, so instead of them getting paid, uh, instead of them paying 1 million, for example, for 10 units, maybe they’ll pay 1 million for. 12 units because they have the, like 20% discounts because they came in early and then afterwards, then the value goes kind of, that’s to incentivize the people to come in early, uh, and then to, to take in more.

Uh, I’ve, I’ve also seen people do v volume discounts where if they invest above a certain amounts, then they’ll get another discount to incentivize people to invest more than less. So, so those are the two, uh, things, and then usually be like discounting the unit price. Mm-hmm. And how do you make that calculation?

In the, in the sheets? Yeah. That’s if you, if you have a differential levels for investors, basically, because I, I, I’ve seen, I have one model that has a water waterfall model. Yeah. That it, it, it has like, uh, multiple tiers, like tier one, tier two, tier three. And probably exact, it looks like I, I didn’t understand it at first until you speak about it now.

And, uh, it has like tier, like 25%, 50%, 75%. I assume these are the discount. And a hundred percent. So tier one is a hundred percent tier two, 75%, tier three, 25%. I assume these are the discounts that you’re talking about and, and depends and depend on, uh, how you define these tiers. And, and, and it’s embedded in the calculation somehow.

Yeah, you could, because there are two ways of doing it. Some people that’ll do it by the, by just having different classes of units and some people would do it based on just discounting the shares. Uh, but it really, it’s the CFAs, like it’s either David or Matt. They’re the ones who can actually make it, I can just talk about it.

But, but they’re the ones who, uh, are actually know how to make it and get the right one. I, I can, I can send you the model that I have, please. It’s like a template, an example, and maybe he can, he can use it and make it happen if, if that’s the right idea. Yeah, please. That’ll be helpful. And then I’ll be able to actually, you know, see it and then say, okay, yeah, how will we do that if you were to do it discount, uh, for those investors, so, mm-hmm.

Useful. Yeah. Okay. Alright. So let me look at the rest of what we have here. All right.

Whoops. Am I on a right screen? Let me go to the right, correct. Screen with waterfall.

Okay. So that’s the finance, which will change as well to add that. So I guess the graph as a bonus, and then the, uh, example discounts. If we were to do a discount. Okay, so then the last one is the securities. So there’s PPM draft and then there’s subscription agreement draft. So this one we went through.

So this one we went through and we just had to, you know, look at everything. Um, overall, this one, this one it talks, uh, go up the top it says 32 million. Although the calculation we made the valuation is about 50 million. Is there a a difference or. Oh yeah. So it’s because, um, so remember when initially we were, we were doing, uh, remember not the first time, not the second time.

The first time we’re doing 32 million. The, uh, yeah, my assistance, they, uh, they used it off the old one. So we, I’ll get my assistance to update it for the new one. Uh, yeah, that, that’s fine. I, if, if there is a type, then we can correct that. I just wanna make sure we are not, uh, we’re on the same page. So this number should be consistent with the evaluation we have in the, in the discount, uh, in the DCF model, correct?

Yes. I think Dave, Dave came up with, uh, enterprise value of 52 million, I believe in, in the model that you just showed right now. Yep. Uh, let me see if I can see it on this in the first one. Yeah. Uh, no, this is a F one. Do you have the other one? Yeah, let me pull it up. Uh, I’ll switch screens. Just one second.

Desktop.

Yeah. Uh, let’s see. The, so if you go to the first, first step. Yeah. You see, uh, I thought yeah, he got like 50 million Yeah. Enterprise value. Yeah. So let’s do it off, uh, 50, I think probably. So that, that number should be consistent with this number, correct? Yes. Yes. That number and then the, the pref that return, or sorry, that number and then whatever pre return we’re going with as well.

Yeah. Okay. I, I like the lower, you know what, and I like 6% is better than, um, than 8%. Like it, it depends because 6% is safer. Uh, for you. It’s safer for, for your dealer. Yes. We’re not promising. But in 8%, besides beside, I’m, I’m, I’m, I’m, I’m the, uh, the shorter stick in the deal because all the deal is, is owned, uh, now is gonna be owned by the investor, not, not the myself.

So he’s sticking the bigger buy than myself. So 6% is what’s a pre is this preference? Uh, percentage, yeah. That’s for, that’s the, um, the minimum. That the minimum return that has to be made, uh, for you to get your fees, because usually if we don’t make at least 6%, then the general partner doesn’t get their fees.

So it’s to make the investors feel safe. I see. Yeah.

So that’s why if it’s low, then it’s like, then you’re really re we’re really relaxing, we’re not stressed. But then if it’s high, it’s good for the, it’s, it’s kind of, it’s like a gamble. It’s kind of like, okay, if it’s high, then they know that they’re gonna do well, but because if they don’t get it high, then they’re not making money.

So it’s a little bit of a, a gamble. I see.

Now, let me ask her a question, uh, while you’re here, we make the evaluation, uh, based on, uh, the 50 million, right? And, and that’s the fund that we raise. Yes. What happen if I was a, if I, if I am able to negotiate a lower price, would that increase my contribution into the fund or am I still bound by that number?

It’s a good question. The, the way that the model is built, it’s taken every, it’s taken everything from the value. So if you were to negotiate, that’s a very good question because I think you can use it to say that, oh, you own this many limited partnership units, and, uh, and you can say, that’s my skin in the game.

That’s one way of structuring it. Because if you say, if, if you’ve already done evaluation and then you’ve told the people to lower the price of the deal despite the evaluation, then you can take that as the skin in the game you have in the deal. Mm-hmm. That, that’s one. And there are different ways you can do it, but that’s one idea.

Uh, because if you do it based on that idea, then when people start Yeah, that’s what that Yeah, that’s what I’m, uh, I start thinking about it. I said, okay, we are raising 50 million based on the evaluation of the company. Now I’m, I’m negotiating with, with the owners and let’s say, uh, they agree to my offer, 32 million.

Right. So that means my skin of the game, instead of of 10% general partnership, it’ll be like 28% instead. And, and therefore that will lower the contribution, that will lower the percentage for the general, uh, for the limited partnership. Would, would you interpret that this way? I, I, I would, I would. The only thing is like, yeah, I definitely, I’ll talk to, to matter, matter purchase.

Uh, I just raised capital, but matter, he bought a business in Vancouver and he closed it similarly. So I’ll talk to him. But, but I, I think it’s best if you have, if, if you can tell, sell the idea that you have skin in the game because that’s an objection that you would get. So, uh, if you were able to, that would be good.

Um, the second thing is that I’ll also ask on what merits did the person, like, why did the person choose to accept your negotiate? Like choose to accept it because. You know, obviously you have the skills and the, and you have your experience, but then it’s like, why? What are the reasons why they would accept losing 20 million?

So we have to really just dig into like, what’s the reason why, um, you know, and then what are, are they are, are they using another evaluation and so on. But I would just, I would just really just take it as skin in the game so that if you mm-hmm. Even, even lenders, um, you can position it that way. And I think that’ll be the best.

Cuz like if you raise a hundred percent other people’s money, it’s, that was another, honestly, it was another thing I was wondering about. It was like, okay, that’s a lot of money to when, when there’s nothing in the game. So I think you can position as more skin in the game. Uh, but those are my thoughts.

Okay. Yeah. Yeah. That, that’s consistent of what I’m thinking. Uh, basically in that, uh, Pedro, my skills and, and negotiating skills are probably, I’ll get a, a lower valuation. Uh, between me and the seller and, and we agreed to it. Although we are, the actual, uh, valuation is based on the, the, the DCF model. It tells us this business, yeah, is supposed to generate that much money and therefore, in the future, and therefore it should be valued at 50 million.

The, the part that if, if I get it at a lower valuation, that means it’s, it’s in my, uh, scales and negotiation and be able to, uh, work out a deal to get the deal funded. Now, if there is a extra money, because of the money raised, we’re gonna raise the full 50 million. It means that, uh, the, the, the units, uh, that’s gonna be maintained, part of part of it’s gonna be paid for the deal.

The other part, it would be. Like working capital or can be used in the business as well. Yeah. You can use it for offer. So it’s not, it’s not, yeah. So it’s not like money. Gotta put it in my pocket. It’s money gotta be included inside the business where the, where money is needed for the business. No ab absolutely.

Yeah. Wouldn’t people do the real estate deals? Was gimme a call when people are doing real estate deals? Yeah, they don’t, they don’t only just raise the money to buy the, the, the apartment they always raise like a little bit for, for opex. So, um, alright. That’s, that’s way to position it. And, um, yeah, no, I think, I think, yeah, I, I think if you, you take it as, and there’s also something that we’ve tried too.

There was a fellow called Zachary, he’s doing a development fund and for him we had it so that we argued, so he didn’t put any cash into his, in his fund. But we just said, okay, so just look at the salaries that you’re getting paid over X amount of years, and then use that to justify why you own this much, um, why you own this much, uh, in the limited partnership.

Um, you know, or sorry, how, why you own this many limited partnership units. So we did something like that with him where we just said, okay, based on your salary, uh, you know, and your sweat equity, this is how much you’ve brought to the deal. And then we just said, basically we we’re taking risk in it. Loan, we, we did all this work and we’re doing all this for this salary in the future.

Mm-hmm. And then we just said that that’s why we’re earning this many units, cuz this units is worth this much in the salary that we’re, that we’re not taking. Mm-hmm. So that was another thing. So you can also consider something like that, but um, but I think next step is who’s this person calling me? But I think the next step is, um, You can use that skin in the game and you can say that, uh, whatever you get, you can convert that into units of the limited partnership.

So when the investors come in, they’re not saying, oh, you know, you didn’t bring anything in. Uh, so that we can get people that are committed as well. I see. Yep. Perfect. Right. Good. All right, ppm, so then the pp basically, if I were to just summarize, this is all fine and this is all really easy for us to do in boilerplate.

The only thing is that for the, um, there are a few things here. So then for the risk factors, um, you know, there’s several things here that we’re not really capable of doing a hundred percent because, you know, we’re not able to like, support in the court of law for the risk factors. So we just have more.

Um, so, you know, we’re not, we have to ask counsel, um, for, uh, state law redemptions and, and if this, like this is more about. Uh, if somebody can take the units out and then they, em it, uh, what are the risks in Delaware law? Mm-hmm. So that’s something that we’re honestly having to research and until somebody is about to close, this is not really needed, but we need, we need, um, uh, we’re, we’re not able to, to do this right now, uh, because we, we don’t have a legal counsel that can do this last risk disclaimer.

So we may either remove it or have to get a alert to finish this one. Um, that’s the one line. And then competitive risks, uh, this one is more easy for us to do the competitive risk and the leverage risks. But yeah, I think, I think for the, uh, for this one, uh, for, for this line, uh, we have to look at this line and this parts mm-hmm.

Uh, in, in the ppm. Uh, but everything else, uh, Finance and strategy. This is all generic that we’ve used for deals that close. So I’m not really worried about the rest. It’s just that, uh, that first piece mm-hmm. That we have to get a lawyer to review and accurate. Okay. Uh, but that, that’s all we did for the, the PPM

markets. So, uh, another question. Are you getting any foreign, um, would you be open to people not in the us I’m assuming so, because you’re already talking to Australia, right? Absolutely. Yeah. Yeah, definitely from worldwide investors. Okay. That’s the best. I, I see a lot of investors like from Australia investing here in the United States because it’s a better market than over there and, and vice versa.

So. Nice. Uh, yeah. We just tap into everybody. Nice. I think I, I looked at your database. It has a lot of, uh, Australian investors listed in there. Uh, I’m not sure if they are active or not. So I’m assuming that they would, they would be interested to invest in US market as well. Oh yeah. They, they definitely would.

But then the most, we’ve just seen, most of the action has been, um, we’ve seen most of the action domestic. And, uh, well, I mean maybe because I’m here, I’ve just see most of the action in, in either west of Canada or, uh, or throughout the United States. And then there were some in UAE that we saw. But, but that’s just me personally.

Uh, and then the rest is more just, uh, I hear people say that there are people active, but I personally haven’t seen it yet. Uh, so that’s just been my personal, uh, take on it. Uh, but other than that, uh, this is pretty much ready for introductions and, let’s see here, property description and address. And then we have to update, so we have to update all these, um, yeah, the offering numbers and, yeah.

Which, which you can do easily. You have a macro to do that, right? Yeah, exactly. We, we, we have some code that just automates, uh, all the find and replaced. Mm-hmm. That’s nice. Yes. Yeah. So last thing is the subscription agreements. This is where when investors read and sign, um, they read this, they agree to this, and

here’s a redundant description of units. It’s a bit redundant because it’s already in the ppm. So we can actually move this referred to ppm.

Okay. And here’s Go on, sir. Yeah, that’s, that’s in the schedules, right? Yes. And so here’s where the investor science and so on, and they do everything here. And then the last thing is to include the, um, the escrow. We, we use north capital for escrow. They’re really good. So we just send the documents to North Escrow.

I think it’s like between 200 and I think it’s around $200. Um, they’ll do the escrow accounts, um, and then you can accept, we can send them the documents, they accept the investors through there, and then mm-hmm. So that’s pretty much the, the, how the process works. Very good. So one, once you complete that, uh, ppm and all these documents, do, do you need to file it with the s e c or you, you don’t need to?

No. So the filing only happens, uh, after the investors invest, uh, because we, so after the first 30 days, after the first investor actually signed the documents and then won a wire mm-hmm. Then we, mm-hmm. We need to do something called, uh, form D with Edgar. So that’s, that’s easier. It’s funny that that’s actually easier than the PPM because the Form D, you’re just saying how much they put, how much money they put in, and then.

Um, and then we can manual do it and we have a bunch of videos explaining it. Uh, yeah, the, it’s harder to do the PPM usually than to do the Form D, um, on Edgar, but that’s usually what we do. Mm-hmm. I see. So, so it happens the sort of filing after the investor come in and, and sign for and specified how many units it’s gonna do and, and wire the fund already to the escrow account.

Correct. And, and, and then following that, then you will have to, uh, file an s a c, uh, the form D uh, for each investor, or you wait until you collect all of them and, and you solve, uh, and sell out all the units and then you file it once that, that’s a good que i, it’s, it’s when you get them all and then you close the offering, because some, it depends on how many closings there are.

So if there’s like one closing. Then you need to file that one closing. Uh, but then if you have multiple closings, then you need to file like for each closing last time we checked. So like, let’s say there’s, um, I wanna show you an example of one. There’s actually one example of somebody that did a, an Edgar filing.

Let me try to get it. Uh, he did with us actually. Um, let me go up here.

Aha. I found one. Okay, just one second.

Is it copy and pasted?

There we go. So let’s see this one. All right. Yeah. So this was somebody that joined just a while ago. Uh, so then last year or two years ago, actually, he filed this one. So let’s see the documents here.

Okay. They reported, all the brokers said what they’re offering.

This one’s a little bit different because it’s for, uh, a red cf. Um, but yeah, we wanted, so then we just filled this all out, like with how all the states that, uh, we want to offer this, the deal in. And then the thing is that we have Form D, they’re doing Form C, which is a bit more, but the idea is like for every closing, uh, we do, it’s like if we bring in one investors for one closing, we do one report.

If we do 10 investors for the another closing, then we do the other. So that’s usually the, the idea in a, in a nutshell. But, uh, here’s the. Uh, lemme look at the documents. It’s just, uh, pitch check. It’s interesting.

Yeah. So you see these are all the documents that are explaining the, the deal. And it’s like Wefunder was like the broker dealer that did this for them, but we don’t need to use a broker dealer because they’re doing Reg C. We’re doing Reg D at Regulation D. So Regulation D, you don’t need to have a broker to do it.

Uh, see, and lemme just check as you see form D.

So here’s the, here’s the official Form D, and I’ll send this to you in the chat. Uh, but here are all the questions we have to go through and fill out. I see. And.

We say the amounts, and then the one that we’re doing is 5 0 6 C is the best one and the cheapest one. Usually these ones are good too, but in these ones you’re not allowed to advertise. So the way, the reason why you’re able, oh yeah. But then the reason why you’re able to do a press release and you’re able to talk and, and all that is because 5 0 6 C you’re allowed to, uh, to do that.

So,

and then this is the, it’s, it is really interesting. So if you use a broker dealer, then you just put in the, or a broker or somebody, then you put in the, um, the percent success fee they’re getting sees, because that’s why we’re, we’re not, uh, we’re not putting people there that are not registered because that’s a problem as long as.

People here are registered to people to do this. Uh, like if you give them presents, then that’s important. So that’s another thing. And then use of proceeds and that’s it. Then you sign it, you submit it, uh, and we can do this and share this with you. And, but then this is only after the investors invest. So I think it’s in the first, uh, 30 days.

Okay. Yeah. Now, what happened if you don’t, uh, are not able to sell all the units? Uh, and there are some units remaining, but can you close the funds at this point or you just continue on, uh, raising the rest of the units? Yeah, so I mean, there, there are a few, few ways. Like some people, they technically as the PPM is like the, the pri, the private placement memorandum.

It says all the things you can do. So, um, really we’re in charge or you’re in charge of like, Of saying the rules of when you can keep it and when you have to give it back. So you’re actually in control of that. But the second thing is it’s based on the minimum amount that you need to do the thing that you said you would do in your business plan.

So if, for example, you’re, you’re, you’re raising, you know, you raise 10 million or maybe even, you know, let’s say you raise 10 million and then it’s shorts of the 32 million. Uh, but you get some other finance here. Maybe there’s some lender, maybe there’s some seller finance or something crazy happens and then you’re able to close it, and then you’re able to carry on in your business plan.

Um, then you would proceed. But then if you raise 10 million and then that’s it, there’s, there’s no one else who can fill in the gap then, then we can’t really do anything. So then you would have, because you wouldn’t be able to do the things that you promised in the PPM or you can’t change it to fit what you want to do.

Mm-hmm. Then you have to give it back. So, so usually the people, usually the people that give the, the capital back or they can’t close it after escrow is because they can’t do what they said they’ll do in their business plan. Because they haven’t raised enough money either from debts or from other ways to acquire the business to do the thing.

So that’s why I see. I see. Yeah. Uh, okay. Uh, I notice also the, uh, the PPM has a limit of 90 days, so you have to raise those, these funds within 90 days. So what happened after the end, the, the end of 90 days and you’re not able to raise all the funds, you just to give the money back, or can you amend the P B M to extend the time?

Sure. So, so two things. Yeah. I mean, the, the current PPM is, um, I mean, as long as it’s in this drafting phase then, and really, really exists from marketing, because I’ve seen deals that we worked on at another investment bank where I was working at, and then we will just say 90 days to say, oh, it’s in 90 days.

But then really it was just marketing. So yeah, I don’t want it to be anything that as much is this, is this when they sign a subscription agreement, uh, and then it says it closes in 90 days. That’s more serious than if we’re just, if nobody has invested yet, can we say in 90 days? So I see. So the, the 90 days is not carved in a stone when you bought it in the pvm, but it is carved in a stone once you, you get the investor sign on and you just need to close within the right days.

Yeah, yeah. Because, because, and then there are different ways. Some people, they, they have it so that the investors have a, uh, a deposit that they put to keep their spots, because some people, they put the money in right away, but then some people, they just say, okay, I’ll commit this much. And then to make sure that they keep their commitment, they’ll put maybe 10% down.

Or 5% down, or even maybe some people, they do nothing. Now they’ll put something down. Um, and then ae who he closed the deal with, he, uh, he didn’t, he, some people they do, they do no refunds for the deposits, but then he, because he was his first deal, he, we, he chose not to do no refunds because he wanted to, he was a new investor and he wanted to keep the relationships with these investors obviously.

So, uh, but then that’s, that’s, that’s your choice. And then, and then afterwards, then it’s like, okay, after, you know, we’re ready to close, you can do something called a capital call where you, you tell ’em, send the rest of the 90% of the money. Now I’m ready to buy the business. So some people do it like that, uh, you know, that’s another way that it can happen.

But the easiest way, honestly, is just to get the, all the capital in and then just to have them commit to all the capital. And if they can’t, then you at least get like some sort of deposits and then call on the rest of the capital as you go. Because remember the way that you did the 60% deal. With this?

Uh, yes. If, if that goes through, it’s, it’s almost the same thing with the investor. Sometimes the investor, they’ll bring in, they’ll say, oh, like, hey, I want to put in just, you know, 2 million now and then I’ll put in 10 million later. It’s say, okay, do that. But then if we find somebody else that would do more, then you know, you would have to forfeit your spot.

So you can just get them to get the down payments and then to agree to do the rest. And if they don’t do the rest, then mm-hmm. They’ll lose their spots. Um, in, in general. So those are just a few things we noticed. Uh, and the last thing is we want to really be, uh, we’ll try to get more than we need.

Because, because we, we can get people that will say, they’ll do 30 and then as you said, that they’ll, people flake. And we see this a lot, people flake. Mm-hmm. So we wanna try to get, maybe it’s even better to try to raise 50 and then we only need 30, you know, maybe that’s better. Cause people are gonna flake.

That’s right. Yeah. All right. So I think, um, yeah, so I think, let me, let me summarize. So I think the next step is, um, uh, number one, it’s the 6%. Let me just write this down so we get on the same page. Whoops. Renty. Okay. Yeah. So, um, so from 8% to 6% graph, uh, graph on, uh, Excel meets the graph on Excel sheet.

Then there was something else. Then there was, uh, uh, the, uh, the fund amount, yes

to.

It was 50. I wanna do 51 million because there was like, it was 50 and a hundred thousand and something. So, yeah. Okay. Um, what else? You, there was something on the pitch deck as well. Uh, the, the one, the one pager or was highlight the geometrics bigger font, the, uh, the pitch deck. Uh, I’m gonna send you my, uh, my profile, company profile.

That has a nice picture you can use there. Yeah. Uh, I think that’s it and then I’ll look over the recording. Uh, last thing is that, uh, Monday, so I’ll cue the,

something important about press releases is that, um, You know, because we’re not saying the terms of the deal, uh, that’s why we’re able to even do it because we’re not supposed to say the, uh, so, you know, the thing about the, the preference and then all this stuff, the deal highlights, so mm-hmm. We’re, we’re, we’re keep, we’re not saying that on the press release.

That’s why it’s safer. Uh, whereas yeah, if, if we’re saying like, oh, you’re getting this much money for the deal, it’s like, that’s dangerous because then you, somebody that’s on credit can see it and then they’ll say, oh, you said somebody that’s not credit. And because raises.com we’re publishing the press release, that’ll be on my head.

Uh, so that’s why, uh, the press release is more, oh, here’s what we’re doing, here’s the revenue, but go to Mamud if you want to discuss, and then it goes right to you. Correct. Yeah. It’s a lot safer. Uh, and, and in terms of credibility as well, so you, you, you, you have flexibility to, uh, arrange or exchange any of the details without being, uh, caught that you are keep changing terms and stuff.

E exactly. Exactly. Yeah. Because things change as you see. Okay. So we can do this. And then I think the, so the next step, uh, uh, so basically we’ll send this and then this will be up for you to approve. And then after you approve, uh, then we do intros. Uh, and note the intros are, they’re good. They’re select.

Uh, we don’t have like a ton. We don’t have a, a huge amount of intros or anything. They’re just very focused and, and few to start. Uh, you know, so then let us know when, and then we can do the select intros, uh, after we send, so basically you approve, uh, are changes above. Then we do select intros.

Cool. So that’s seems to be it, but um, So Diana answer, how, how does it work? Is this just like one, one zoom call with everybody on, on the line, or it’s just one-on-one? Yeah. So it’s all one-on-one. So what we do is, is really just an email introduction because they’re very, they’re very old-fashioned, so, you know, they’re not comfortable with, uh, uh, anything too crazy.

So we just do a, an email introduction. Say, oh, we say, here, here’s my mood. He’s, he’s, uh, you know, he, he, he jumps onto razors.com. He has a deal that could fit in your, uh, mandates, you know, once you to discuss, feel free to connect and explore. And then from there, then, you know, we get Frank, we get Frank Camille, uh, uh, what’s it called, Sean, because your deal is above 25 million.

We have, we’ll probably have at least, you know, probably at least five. Like on Monday, uh, we can move really fast. Mm-hmm. And then there’s just a discussion. They’ll say, okay, send me this, or Let’s discuss this. But then the idea is to get the, um, To get on the phone and then to say, okay, hey, what, what’s your type of, uh, I guess what are you, what’s your investment criteria?

What, what do you, uh, to get information on them? Uh, then they’ll say, okay, yeah, I’m looking for this. And then you have it already. Yeah, we have this type of deal. Uh, what do you like to know? Happy to answer any questions. And then, is this really question and answers? Uh, because they already, they already know us, so it’s already easier because they’re like, okay.

Yeah. It’s from, it’s it’s raises.com people. Okay. Yeah. So then they’re really, the guards are down. Um, so it’s more just a normal human conversation to know what they’re looking for and then to answer any questions about your deal. And then after the call, then, uh, unless they ask for it right away after the call, then we can send the, uh, the pitch decks and then all the information.

I see. So, so usually, so it’s a software probe with the email, and if they’re interested, then it’s just in. One-on-one, uh, answering questions and, and I followed up with sending them the details, which their comes e Exactly, exactly. I think the best one for you. There’s a company called, uh, Cambridge Wilkinson.

Uh, they’re the best com. They’re one of the best, uh, bankers that we know. Uh, they don’t charge anything. Uh, they charge, uh, they accepting success fee, but then they, they reject 99, I think they reject like 90% or, or all the deals, but we’ll try to get you with them. Uh, they’re a really good company. I love that company, so hopefully we get with them.

Okay. Sounds good. All right, good. All right. So af after to hop up for the next one soon. But any, any other questions before we, um, we get this, uh, uh, yeah, I want, I wonder how, how can you help me with that deal in Australia right now? Is there any. Uh, he will, uh, who can make introduction to, or kind of like, uh, engage in, uh, compensation or, or raise some interest if they are interested to, uh, to fund deals in Australia.

Yeah. So I have somebody in the UK and he’s more connected to that side of the world. Uh, so then if somebody in the uk, but then the, the question too is like, how much is he raising and is it the equity or the debt? It’s the equity, right? Uh, it’s a debt. Oh, debt. But then debts is much, uh, is much better. Uh, I’ll try.

Okay. So today, today we can try. Uh, Kevin, I don’t know if you have time to, the timing will be weird, but Kevin on Yinka, uh, he’s probably the, the best guy for that. Kevin? On Yinka. On Yinka. And then there’s Frank, uh, lending Capital Nets. So yeah, there’s somebody called Frank. He has a lot of global lenders.

And, uh, don’t look at his website because we, he doesn’t really talk about his global lenders on his website. So Frank is really good, and we’re working on a few deals with Frank. Kevin is good at two for debts. Uh, so, um, so we can start those introductions. The only thing is like, uh, I don’t want to take away from this other deal too, because they No, no.

Yeah, we’re just gonna battle both of them at the same time. Well, the Australian dean is very tiny compared to this one, so, okay. Well, well, I have an idea. I, I have an idea. So what, what we can do is like, you can just try to say that, oh, we have multiple, yeah, we have this big deal and we have multiple deals because some people that, uh, we talk to them, we talk to the investors, we tell them to say, oh yeah, just say we have a lot of big deals.

Uh, I just wanna see which one is most relevant, uh, for what you’re doing. And then if they say, okay, we only do our, we we’re only doing more lending this month. Then you can bring in the other one. And if you say, okay, yeah, we end that, then you can bring in the big one and then as an aside, you can bring in the second one.

So we can, we can just do it like that if you like. Yeah, yeah. Whatever works. Right. It’s like a It is, it’s an art. Um, well, funding and, and financing is, is an art by itself. Yeah. Well, anything, dealing with human beings is always an art for sure. Yeah. Yeah. Alright. Alright. Good. So it is nice to, nice to, um, have a trip.

Thank you so much. Uh, I’m, I’m leaving tomorrow actually going to Okay. Youe. And, uh, so I’ll, I’ll, I’ll see you on, on the other side by Monday, uh, Rey for action. And, uh, we’ll, we’ll go from there. Perfect. See what we can, once we make these introductions, I’m, I’m sure there’s gonna be a lot of actions, uh, taking place.

So we’ll see. We’ll go from there. Absolutely. Yeah. So look at either probably today, this weekend, we’ll do the, the changes and then we’ll be ready. And then by Monday we’ll, we’ll send out everything and, and it’ll be ready to go. Okay. So, sounds good. All right, sir. Thank you for your, uh, for your business.

We, we’ll talk soon. All right. Thank you, Natu. Have a good weekend. You too. Cheers.

Content Restricted! You are not logged in.

- If you are a member, check your email

- Then login at Raises.com/login

- Non-members: book us below

What are these calls about?

At Raises.com, we work with thinker-doers who are setting up new funds or acquisitions.

We work together to solve their problems in closing their transactions.

This is for you if:

1. You need:

- To urgently want to set up a fund, or commence a larger acquisition

- Help finishing the legals/financials/securities to prepare a fund or acquisition and also as well as raising capital for one

- Have already invested in and/or syndicated minor real estate transactions but have not done a $10m+ transaction

2. Struggle with:

- Minor profit margins on small deals or syndications and want to work on larger transactions (funds or acquisitions)

- The unknowns, and lack of visibility from the complex world of high-finance to set up and close your transaction

- Allocating time and resources while preparing and executing a sophisticated, large capital raises

- Building relationships with investors with the mandate to finance your fund or acquisition

3. This is not for those who

- Work on pre-revenue prototypes or no-asset deals

- Have all the legals/financials/securities prepared

- Are not principally in US, Canada, UK, or Australia

If Accepted, You Will

1. Join masterminds

- Prior to joining Raises.com, many of our future members have never raised, more than $1m-$2m,

- nor do they have trusted institutional relationships on the debt or equity buy-side for eight-figure transactions.

- So, the same day that somebody joins Raises.com, we integrate members with Raises.com’s JV partners

- who are either investment banks or family offices, who can directly prepare and complete your raise.

- The result: you have a network of eight-figure plus capital raisers with whom you can build lifetime relationships and raise your standards

2. Ready Your Raises

- Prior to onboarding, many of our future members have may not have their information ready for an institutional capital raise ($10m+).

- For instance, many haven’t done a Reg D in the US, or complaint exempt offering in Canada, Australia, or other prominent commonwealth nations.

- Our consultants and chartered financial analysts can assist you in all the financial, compliance and legal paperwork

- to get members 95% through to completion so that you have the compliant offering,

- you have a personal CFA, (Charter Financial Analysts), to assist you with the financials,

- and testing all assumptions therein if needed on a 1-on-1 basis.

- The result: you have a clear pathway to having everything compliant and so you have as many routes to go as possible, even possibly going public with support along the way.

3. Start Raising

- Prior to onboarding, many of our future members have may not the contact information on investors with

- the same mandate, a team to delegate the capital raising to, and a system

- to predictably and quantifiable measure performance to get closed term sheets more systematically for an institutional capital raise ($1m-$100m).

- Many CEO’s do not have the time to be able to go out and do consistent outreaches and measure all of the metrics and do all proper reporting,

- so Raises.com has consortiums of trained appointment setters that are trained to assist you in hitting the markets

- by contacting the tens of thousands of investors from the offices, private debt providers, and so on,

- on our proprietary portal, underneath your company through the compliant structure securities council have created.

- The result: The capital raising process in your organization is systemized and delegated

4. Systematize, Delegate and Repeat

- With an extra set proprietary tools that can be delegated for somebody else to do, or you can do directly, for you to get, investors that even in our network.

- Leverage Raises.com’s online reputation into your capital raise for added traction.

- The result: countless avenues to continue to generated conversations.

5. Get added to the numbers

Raises.com has assisted firms in creating fund and acquisition vehicles for hundreds of people and raising

and closing an excess of $152m in under two years through direct, compliant channels. You will be added to the head count of raises closed.

Raises.com offers licenses for a select group of people to access a membership for a year.

We begin by mapping out a customized process for your raises from set up through to completion.

If someone qualifies for a membership, it will include:

- Raises.com branded creation of packages for all points in the transaction process

- (to convince sellers to be originated, to convince buy-side firms to take part)

- Trained remote staff and teams to work under your company during your raise

- Tens of thousands of compliant vetted investor contacts and data (equity or debt) updated weekly

- Software to autonomously build relationships with investors

- Resources, training and recorded conversations from mastermind members

- Private mastermind communities of principals raising $1m to $100m and beyond

- Capital raising-trained Chartered Financial analysts to finish your documents in as little two weeks

- Warm relationships to FINRA registered broker dealers, council, private equity firms and family offices

The price for annual membership is currently in the upper 4-figure range for those that qualify.

[/um_loggedout]